Introduction

With key interest rates remaining high, raising debt remains costly for companies, prompting them to seek new avenues for investment. History shows that preferred shares (also known as "prefs" in market parlance) can be an effective fundraising tool. They have repeatedly replaced debt financing, helping issuers and investors in difficult economic times. Currently, the preferred shares market accounts for, according to various estimates, 5 to 10 percent of the capitalization of the Russian public equity market. According to Moscow Exchange, preferred shares from 48 different issuers are currently available for purchase at Moscow Exchange-organized trading. In a series of posts dedicated to preferred shares, we will explore the origins and evolution of preferred shares, from the first shares with a fixed dividend yield to the present day.

The Origins of Preferred Shares as an Alternative to Debt Financing

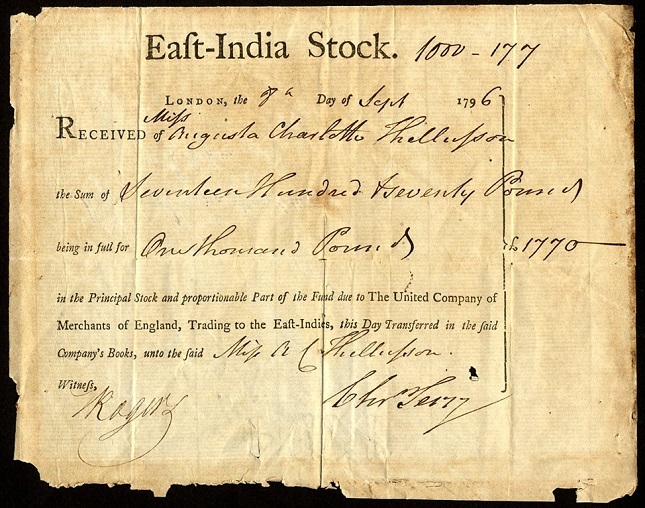

The history of preferred shares dates back to the early 18th century. Preferred shares were initially used as a financial instrument by maritime trading companies. Among the first financial instruments similar in nature to preferred shares were the shares of the British East India Company, issued in 1702. Paradoxically for modern readers, these shares entitle holders to receive dividends not from the British East India Company itself, but from the British state, amounting to 8% of the par value of such shares annually.

With key interest rates remaining high, raising debt remains costly for companies, prompting them to seek new avenues for investment. History shows that preferred shares (also known as "prefs" in market parlance) can be an effective fundraising tool. They have repeatedly replaced debt financing, helping issuers and investors in difficult economic times. Currently, the preferred shares market accounts for, according to various estimates, 5 to 10 percent of the capitalization of the Russian public equity market. According to Moscow Exchange, preferred shares from 48 different issuers are currently available for purchase at Moscow Exchange-organized trading. In a series of posts dedicated to preferred shares, we will explore the origins and evolution of preferred shares, from the first shares with a fixed dividend yield to the present day.

The Origins of Preferred Shares as an Alternative to Debt Financing

The history of preferred shares dates back to the early 18th century. Preferred shares were initially used as a financial instrument by maritime trading companies. Among the first financial instruments similar in nature to preferred shares were the shares of the British East India Company, issued in 1702. Paradoxically for modern readers, these shares entitle holders to receive dividends not from the British East India Company itself, but from the British state, amounting to 8% of the par value of such shares annually.

Common share of the British East India Company. No photographs of the preferred share were found. Source: https://www.scripoworld.com/records/india/east-india-company/.

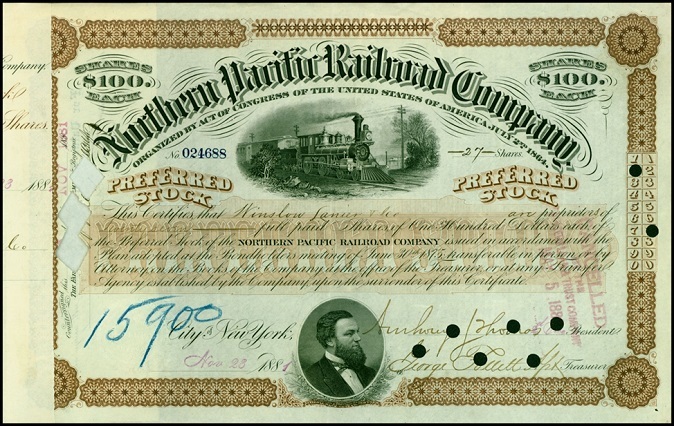

The demand for preferred shares exploded in the late 18th and early 19th centuries. At the time, preferred shares were issued by British utility companies (companies providing gas and electricity to households and businesses, as well as water companies), as well as by companies that used the proceeds from sales to finance the construction of railways and canals. Infrastructure construction is a long-term project, and therefore investments in it cannot generate short-term returns. Moreover, the small size of the stock market and currency restrictions forced companies to attract investment in the region where the project was being implemented. The popularity of preferred shares at that time was largely due to the difficulties in raising debt financing. In 1836, the British Parliament established a mandatory debt-to-equity ratio of no more than 1:3, which deprived many companies of the opportunity to raise bond debt. Consequently, preferred shares became a substitute for bonds, as they allowed them to bypass the debt-to-equity requirement. Moreover, they made it possible to reduce the risk of bankruptcy, since the payment of dividends required a decision from the issuing company.

However, attracting investment at the time remained a difficult task. Companies attempted to enhance the investment appeal of preferred shares in two main ways: issuing shares at a discount or establishing a preferential right for their holders to receive dividends. The preferential right to receive dividends became more widespread and made preferred shares a sought-after instrument, becoming one of the defining characteristics of preferred shares for future years. Furthermore, the fixed interest rate provided by preferred shares acted as a coupon, and the liquidation quota was often paid to preferred shareholders with priority over other shareholders, further enhancing their appeal to conservative investors. In particular, preferred shares were used to finance the construction of the Edinburgh-Dalkeith railway and the Oxford Canal.

The demand for preferred shares exploded in the late 18th and early 19th centuries. At the time, preferred shares were issued by British utility companies (companies providing gas and electricity to households and businesses, as well as water companies), as well as by companies that used the proceeds from sales to finance the construction of railways and canals. Infrastructure construction is a long-term project, and therefore investments in it cannot generate short-term returns. Moreover, the small size of the stock market and currency restrictions forced companies to attract investment in the region where the project was being implemented. The popularity of preferred shares at that time was largely due to the difficulties in raising debt financing. In 1836, the British Parliament established a mandatory debt-to-equity ratio of no more than 1:3, which deprived many companies of the opportunity to raise bond debt. Consequently, preferred shares became a substitute for bonds, as they allowed them to bypass the debt-to-equity requirement. Moreover, they made it possible to reduce the risk of bankruptcy, since the payment of dividends required a decision from the issuing company.

However, attracting investment at the time remained a difficult task. Companies attempted to enhance the investment appeal of preferred shares in two main ways: issuing shares at a discount or establishing a preferential right for their holders to receive dividends. The preferential right to receive dividends became more widespread and made preferred shares a sought-after instrument, becoming one of the defining characteristics of preferred shares for future years. Furthermore, the fixed interest rate provided by preferred shares acted as a coupon, and the liquidation quota was often paid to preferred shareholders with priority over other shareholders, further enhancing their appeal to conservative investors. In particular, preferred shares were used to finance the construction of the Edinburgh-Dalkeith railway and the Oxford Canal.

An example of a preferred share of the American Northern Pacific Railway Company from 1881. Source: wikimedia commons.

Thus, in the 18th and 19th centuries, preferred shares served as a substitute for debt financing, which was not always possible due to legal restrictions on debt-to-equity ratios. They were in demand primarily by public utilities and companies constructing railways and canals. A significant advantage of preferred shares was that they allowed investors to defer income payments during the implementation of a long-term project, reducing the risk of default and bankruptcy.

In the next post, we will discuss the development of preferred shares in the 20th century and their place in the modern world. We will illustrate how the range of applications for which preferred shares were used has expanded and highlight the current state of the preferred share market.

Thus, in the 18th and 19th centuries, preferred shares served as a substitute for debt financing, which was not always possible due to legal restrictions on debt-to-equity ratios. They were in demand primarily by public utilities and companies constructing railways and canals. A significant advantage of preferred shares was that they allowed investors to defer income payments during the implementation of a long-term project, reducing the risk of default and bankruptcy.

In the next post, we will discuss the development of preferred shares in the 20th century and their place in the modern world. We will illustrate how the range of applications for which preferred shares were used has expanded and highlight the current state of the preferred share market.